They are not the same thing — and confusing the two can have serious consequences for your rights to your own home.

It happens more often than you might expect. A client walks into my office, grieving, stressed, or in the middle of a family dispute, and they say it: “But I’m on the mortgage. Don’t I have a right to the property?”

The short answer? Not necessarily. Being on the mortgage and being on the title are two completely different things, and understanding that difference could be one of the most important pieces of legal knowledge you ever pick up.

What is a mortgage?

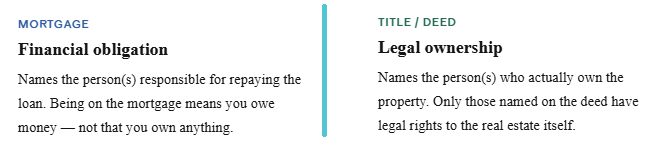

A mortgage is a loan. When you sign a mortgage, you are agreeing to repay the lender, typically a bank, for money borrowed to purchase a home. If you’re on the mortgage, it means you are financially responsible for that debt. You are obligated to make payments. You can be held liable if payments are missed. Your credit is on the line.

That’s it. The mortgage says nothing about who owns the property.

What is title?

Title is ownership. The title to a property, reflected in the deed, is the legal document that establishes who actually owns the real estate. Whoever is named on the deed has legal ownership rights to the property: the right to live there, sell it, transfer it, or leave it to someone in their estate.

Why does this happen?

Sometimes it’s intentional… one spouse has better credit, so they go on the mortgage alone, while the deed is titled differently for tax or estate planning purposes. Sometimes it’s an oversight at closing. Sometimes one party doesn’t realize what they’re signing. And sometimes, unfortunately, it’s not an accident at all.

Whatever the reason, the result is the same: someone is paying for a home they may not legally own.

Real-world example: A husband and wife purchase a home together. The mortgage is in both names. But at closing, only the husband’s name is placed on the deed. The wife is legally obligated to pay, but has no ownership interest in the property. If he dies without a Trust, or they divorce, she could face serious legal hurdles to claim anything.

Things to look out for aka RED FLAGS

- You signed loan documents but were not present at the closing for the deed.

- You have never personally reviewed the recorded deed.

- The property was purchased during a marriage or partnership and only one person’s name appears anywhere.

- You assumed that being on the mortgage meant you were on the title.

The deed is a public record. You can (and should) request a copy from your county’s property appraiser or clerk of court. In Florida, this information is often available online. Look specifically at the names listed as grantees on the most recently recorded deed.

How to handle it

If you discover that you are on the mortgage but not on the title, here is what you should do:

- Pull the recorded deed from your county’s public records and confirm exactly whose names appear as owners.

- Consult with a real estate or estate planning attorney to understand your current legal position and what rights, if any, you may have.

- If the omission was a mistake, the titleholder may be able to execute a new deed (such as a quitclaim deed) to add you as a co-owner.

- If the situation involves a deceased person, you may need to open a probate or ancillary proceeding depending on how title was held and whether a will exists.

- If the property is part of a marital dispute, speak with a family law attorney in addition to an estate planning attorney; property rights in divorce are governed by different rules than probate.

The bottom line

The mortgage tells the bank who is responsible for the loan. The deed tells the world who owns the home. They can, and sometimes do, name different people. If you have never looked at your deed, now is the time. And if something doesn’t look right, don’t wait to get it sorted out. These things rarely get simpler with time.

If you have questions about your property, your estate, or how to protect what you’ve worked for, my office is always here to help. 🙂